Arizona VA loans provide Veterans and surviving spouses great home loan options to purchase, refinance or renovate their home. In fact, VA home loans offer 0% down payment2, have no monthly mortgage insurance and provide competitive interest rates.

Phone: 602.435.2149

Email: Team@JeremyHouse.com

Arizona VA Home Loan

VA home loans give veterans excellent mortgage options and benefits. Eligible surviving spouses also have access to VA loan products. As a veteran, you may have questions regarding your VA mortgage options. The Arizona VA mortgage section of our site will help you learn more about the following:

- Your VA home loan eligibility

- Benefits of a VA home loan

- VA loan qualification*

- VA home loan options

- History of the VA home loan program

Understanding your VA mortgage options is important. While VA mortgages often best suit veterans, knowing if a VA loan is right for you is key. In fact, learning about VA home loan features is a great starting point.

Phone: 602.435.2149

Email: Team@JeremyHouse.com

VA Mortgage Benefits

Veterans benefit greatly from utilizing their VA home loan options. From no down payment to great interest rates, VA is an excellent mortgage option. For example, VA provides veterans with:

- $0 Down Payment

- Flexible Credit Guidelines

- Competitive Interest Rate

- Use VA Loan Multiple Times

- Veterans Can Have Multiple VA Loans At a Time

- No Pre–Payment Penalty

- Loan terms include 5yr Adjustable Rate Mortgages, 15 and 30 year fixed3

Arizona VA Home Loan FAQ’s

Max VA Loan amount is $2.5 million

In most cases no down payment is required.

No, Monthly mortgage insurance is not required. However, some veterans pay a “VA Funding Fee“

Yes, VA allows seller and gift funds to pay for closing costs. Similarly, VA permits sellers to pay for eligible consumer debts of the veterans.

VA loans finance primary residence single family, town-home, condo or manufactured homes

Phone: 602.435.2149

Email: Team@JeremyHouse.com

VA Home Loan Qualification

Mortgage loan qualification is what starts the homebuying process. You’ll provide information on your credit, income, assets and debts so we can give you an estimate of the size of a loan you can afford. There’s never a charge to get qualified with us. Veterans reap several benefits from completing these 4 easy steps:

- Complete Home Loan Application

First, a home loan applicationopens PDF file is completed on the phone or online and typically takes about 10-15 minutes.

- Provide Lender with Supporting Documentation

Next, supporting documents veterans submit documents such as pay-stubs and bank statements. These help us verify that the information on your application also meets underwriting guidelines.

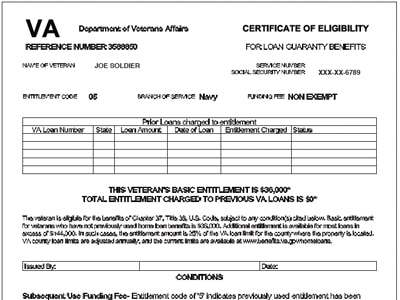

- Determine VA Eligibility

This step marks the difference between VA and non-VA qualification. We order a VA Certificate of Eligibilityopens IMAGE file confirming your VA eligibility (or “entitlement”) is sufficient.

- Lender Reviews all Documents

Finally, after reviewing your documents, information and VA entitlement your qualification is complete.

{kind=link}

Phone: 602.435.2149

Email: Team@JeremyHouse.com

Types of VA Home Loans

VA offers veterans several home loan options. The different loan types include purchase, cash out refinance2, streamline refinances, non cash out refinance and VA Renovation loans.

Purchase Loan

A common use of a VA mortgage is to finance the purchase of a new home. Veterans utilize VA home loans for the purchase of both a resale/existing homes as well as a newly constructed/new build home.

Refinance (non Cash Out)

Another benefit of VA home financing is the non cash out refinance option. VA offers 2 options to refinance without taking cash out.

- Streamline Refinance (called an Interest Rate Reduction Refinance Loan or “IRRRL”)

- Full qualification Rate and Term Refinance

Streamline refinances lower the interest rate of an existing VA mortgage while keeping the term of the loan the same. For example, a 30 year loan refinanced into a new 30 year loan at a lower rate. VA streamline refinances require no appraisal. Additionally, VA streamlines require no income / asset documentation from the veteran.

Full qualification VA Rate and Term refinances allow veterans in the following situations to refinance without pulling cash out of their home:

- veterans not eligible for a VA Streamline

- refinance and change the term of their existing loan.

- refinance a non VA mortgage into a VA mortgage.

Cash Out Refinance

Veterans also have the option of doing a cash out refinance using their VA home loan. You will receive a lump sum of cash that you can use however you like. Common uses for this cash include other purchases, investments, debt consolidation, home improvements and more.

Renovation Loan

VA Renovation loans (also see VA Escrow Hold-backs) help veterans rehab either their current home or a home they are purchasing. Using future value in determining the VA Renovation loan makes this loan product unique. In fact, the value comes from the appraiser stating the homes worth as it will be once the renovations are complete.

Phone: 602.435.2149

Email: Team@JeremyHouse.com

History of VA Home Loans

“VA” stands for Veterans Affairs. Initially, the VA began insuring home loans for veterans in 1944. Ultimately, the VA’s focus was to combat the aftermath associated with war. Interestingly, the VA does not fund, approve or close VA Home Loans. However, the VA creates rules that Arizona VA mortgage lenders follow.

In addition, VA insures each VA home loan. In fact, this is what allows lenders to provide veterans this amazing home financing option. To date, the VA has insured over 18 million VA home loans.

35/1 ARM – Interest rate is fixed for the first 5 years. Beyond the 5 year mark, the rate can change once every year for the remaining life of the loan. When the rate changes, your monthly payments will change relative to the direction of the rate change.

37/1 ARM – Has a fixed interest rate for the first 7 years. After, the rate can change once every year for the remaining life of the loan. When the rate changes, your monthly payments will change relative to the direction of the rate change.